Is Your Luxury Home Truly Protected—Or Just "Covered"?

If your home features custom architecture, rare finishes, high-end systems, or valuable collections, you might assume that your current insurance policy protects all of it. But are you sure?

What most high-net-worth homeowners don’t realize is this: standard home insurance often stops short of what it takes to fully restore a distinctive home after a disaster—especially one involving floods or custom features.

In this article, you’ll see the side-by-side reality of a catastrophic loss at a luxury waterfront mansion—comparing how a standard policy fared versus how a high-value policy could have protected the property (and the lifestyle) more completely. We’ll also give you the four critical questions to ask about your current coverage.

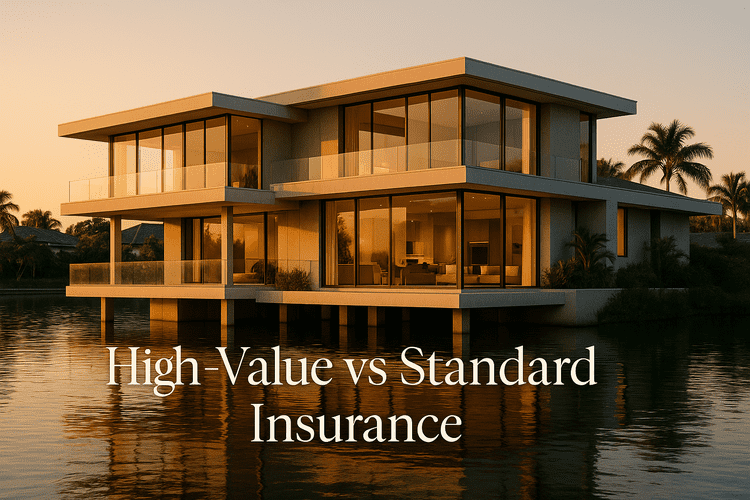

Case Study: How a Coastal Luxury Mansion Exposed Gaps in Standard Insurance

Property Overview

This 9,400-square-foot modern waterfront estate included:

Floor-to-ceiling glass walls

Imported stonework and hardwoods

Curated art and wine collections

A smart home system and private dock

Its replacement value far exceeded local averages—but the insurance didn’t reflect that.

The Coverage Decision

The owners opted for a standard homeowners policy, lured by lower premiums. The coverage:

Used actual cash value (ACV) instead of replacement cost

Included basic flood protection

Had limited personal property coverage not customized for high-value contents

The Storm That Changed Everything

A once-in-a-century flood devastated the property:

Water breached the sea wall and flooded every floor

Custom cabinetry, imported finishes, and smart systems were destroyed

Art, wine, and collectibles were ruined beyond recovery

Filing the Claim: Where Standard Coverage Failed

Here’s what happened when the owners filed a claim:

Depreciation reduced payouts significantly.

Because the policy used actual cash value, items were reimbursed for far less than their replacement cost.

Flood endorsement fell short.

Basic flood protection didn’t come close to covering structural and interior damages.

Custom features weren’t covered.

Many finishes and valuables weren’t itemized or scheduled—and were excluded.

The result? Over $1.2 million in out-of-pocket costs and delays that left the owners displaced for months.

Standard vs. High-Value Home Insurance: 5 Key Differences

1. Valuation Method

Standard Policy: Uses actual cash value or capped replacement—meaning depreciation reduces claim value.

High-Value Policy: Includes guaranteed replacement cost, covering full rebuilds without depreciation or inflation limits.

2. Coverage for Custom Features & Valuables

Standard: Pre-set limits that don’t reflect rare materials or valuable collections.

High-Value: Custom appraisals ensure adequate limits for everything from imported stone to curated art.

3. Exclusions and Flexibility

Standard: Often excludes emerging risks like cyber threats, water backup, or custom architecture.

High-Value: Offers flexible endorsements for flood, wildfire, cyber liability, and even antique furnishings.

4. Additional Living Expenses (ALE)

Standard: Covers basic hotel costs—but often falls short for long-term displacement.

High-Value: Includes premium housing, private storage, and lifestyle continuity support.

5. Claims Experience

Standard: Generic adjusters, slow timelines, and frequent disputes.

High-Value: Concierge claims service with specialized adjusters trained in complex, high-net-worth losses.

What Would Have Happened With High-Value Insurance?

Had the owners selected a high-value policy:

Full rebuild costs would be covered—no depreciation.

Art, collectibles, and luxury finishes would have been itemized and reimbursed.

They’d have received premium temporary housing and relocation support.

The claims process would be managed by a specialist team, with faster resolutions.

Instead of trauma and financial stress, they would have experienced a professional, streamlined restoration.

4 Critical Questions to Ask About Your Current Coverage

Before disaster strikes, make sure your insurance answers these:

Does my policy guarantee full replacement cost—without depreciation?

Are my custom features, collections, and finishes specifically covered?

Is flood, wildfire, or other relevant risk protection included?

Will I have a dedicated claims team experienced in high-value losses?

Conclusion: What This Teaches Affluent Homeowners

After facing a $1.2M shortfall, these homeowners learned a hard truth: standard policies simply aren’t built for exceptional properties.

Now that you’ve seen the real difference a high-value policy can make, it’s time to look at your own coverage and ask: If this happened to me—would I be fully protected?