Schedule Fine Art Insurance in Milton, GA — PURE vs Chubb Compared

STAR — A spring microburst shattered the skylight of a Birmingham Hwy studio, soaking a $60 000 canvas.

STORY — The owner’s standard HO-3 capped “collectibles” at $5 000, forcing a painful out-of-pocket restoration.

SOLUTION — Schedule fine art under a private-client Valuable Articles policy. Below you’ll see exactly how PURE and Chubb stack up for Milton collectors.

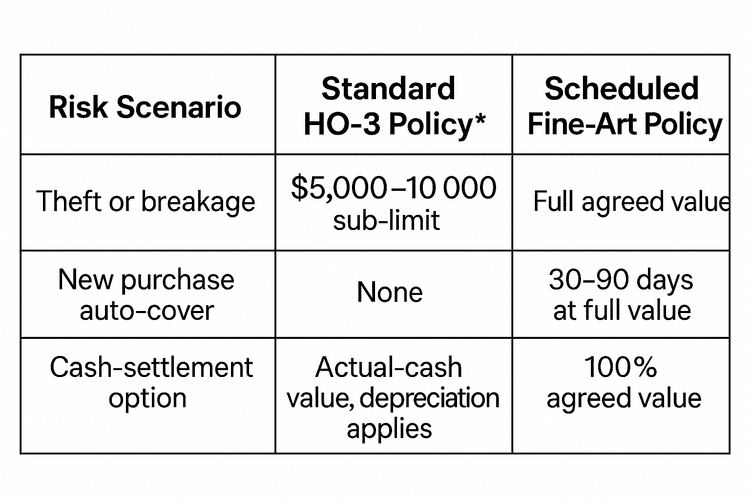

1 · Why “Scheduling” Fine Art Beats Standard Coverage

*Georgia ISO HO-3 specimen form; caps vary by carrier.

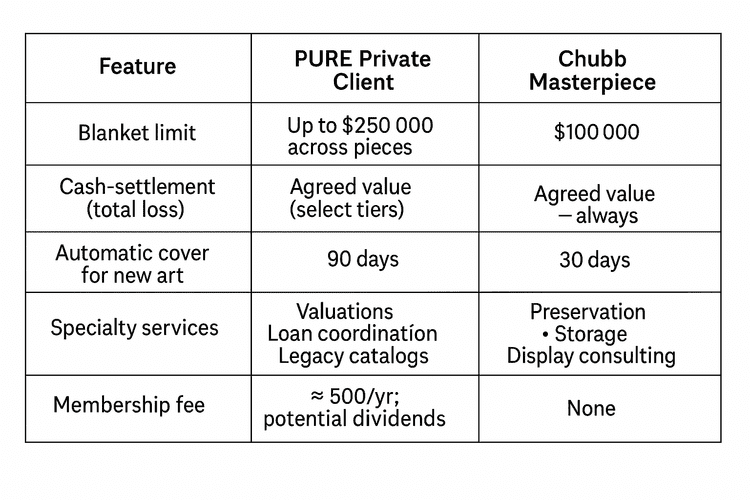

2 · PURE vs Chubb — Feature-by-Feature Comparison

Choose Chubb if guaranteed cash-settlement is your top priority. Choose PURE if you buy & sell frequently and value a longer auto-cover window.

3 · How to Schedule Art in Three Simple Steps

- Appraisal / Invoice — send us a PDF or clear photo. (No appraisal needed if piece < $250 000 and using PURE blanket.)

- 30-minute Private-Client Art Audit — we complete the application and select carrier.

- Issued Endorsement — you receive an agreed-value schedule with zero deductible.

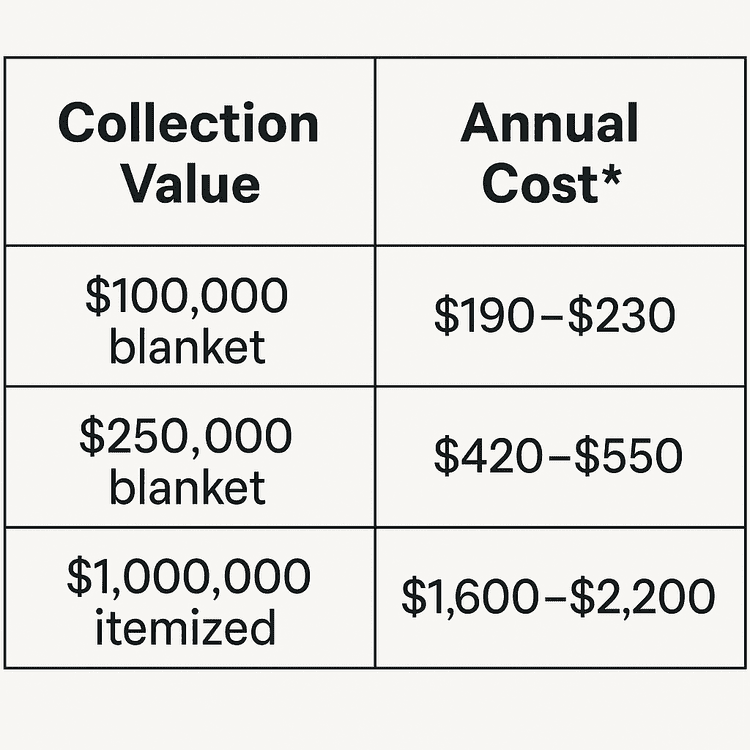

Milton Fine-Art Scheduling Costs (Typical 2025 Rates)

*PURE & Chubb GA filings; assumes central-station alarm credit.

4 · When to Upgrade or Switch Carriers

- Any single piece is ≥ 10 % of your homeowners dwelling limit.

- You acquire > $100 k in new art within 12 months.

- You loan art to galleries — transit limits differ.

- You want guaranteed cash instead of repair / recreate.

Schedule My Art in 30 Minutes →.

Frequently Asked Questions

Do I need an appraisal for every piece?

Only if an individual piece exceeds \$250 000 or if you choose itemized coverage. PURE’s blanket option lets you declare combined value up to \$250 k with photos.

Does scheduling art raise my homeowners premium?

No. Scheduled art sits on a separate Valuable Articles policy, leaving your HO-3 or HO-5 premium unchanged.